.jpg)

Where is the Return on Investment?

For all the noise surrounding AI adoption, one question continues to grow in importance: “Where is the return on investment?” It is a deceptively simple query, yet one that elicits radically different answers depending on which executive you ask, which analyst you cite, and which layer of the organisation you examine. Never in recent technological history has a capability been deployed so broadly, so quickly, and yet been measured so inconsistently.

And that inconsistency matters. It shapes board-level confidence, budget cycles, transformation ambitions, and the capital of the Chief Data & Analytics Officer. The credibility of data leaders hinges increasingly not on whether AI is adopted, but on whether its value can be demonstrated with the clarity and discipline expected of any other enterprise investment. In short: the era of experimentation is declining, as the era of evidence becomes increasingly needed.

A wave of new research from management consultancies, academic institutions, vendors, and enterprise usage datasets offers the most complete picture we’ve had to date of what AI is actually delivering inside organisations. And while the attention-grabbing headlines can make your head spin, when you place these findings side by side, a clearer narrative emerges. AI is generating value, often material and sometimes transformative. But the distribution of that value is extraordinarily uneven, the measurement regimes are inconsistent bordering on incoherent, and the distance between pilot-level enthusiasm and CFO-grade validation remains wide.

This article brings together the latest credible sources to examine the state of AI ROI with the seriousness this moment demands. The goal is simple: to help senior data leaders understand what the market is really telling us, where the gaps lie, and how enterprises should be measuring ROI if they want the next twelve months to look less fuzzy than the last.

The rise of AI adoption and the reality behind the hype

Every major report agrees on one thing: enterprise AI adoption is no longer tentative. It is accelerating with a force that is reshaping organisational workflows, technical architectures, and the lived experience of knowledge work. Whether it’s being forced from the top down, driven by an innovative Chief AI Officer, or coming bottom up (with black-box AI running rampant), AI is here and it is now part of the new normal.

OpenAI’s State of Enterprise AI 2025 makes this clear. ChatGPT Enterprise seat deployment has grown nearly 9×, weekly message usage has increased 8×, and year-over-year growth in reasoning token consumption (a proxy for deeper, more complex workflow integration) has expanded by an astonishing 320×. These are not the metrics of lightweight experimentation. They describe an enterprise environment in which AI is rapidly becoming embedded into the routine flow of daily work, both for individuals and for the systems that support them.

Survey data from Google Cloud’s The ROI of AI 2025 reinforces this picture of acceleration, while also adding important nuance. Across a global sample of more than 3,400 senior leaders, nearly three quarters now report ROI on at least one generative AI use case, with most achieving payback within the first year. This suggests that AI is not only being adopted at scale, but is increasingly expected to justify itself on commercial terms.

The report’s worker surveys reinforce the operational shift underway. 75 percent of enterprise users report improvements in the speed or quality of their work. Most attribute 40–60 minutes of time saved per active day to AI, rising to 60–80 minutes in technical fields such as data science and engineering.

And yet, as impressive as these numbers are, they do not resolve the central tension: why do so many enterprises still struggle to demonstrate financial ROI? With deployment happening at such speed, do leaders even have the time, or the operating discipline, to collect the data and translate productivity into pounds or dollars?

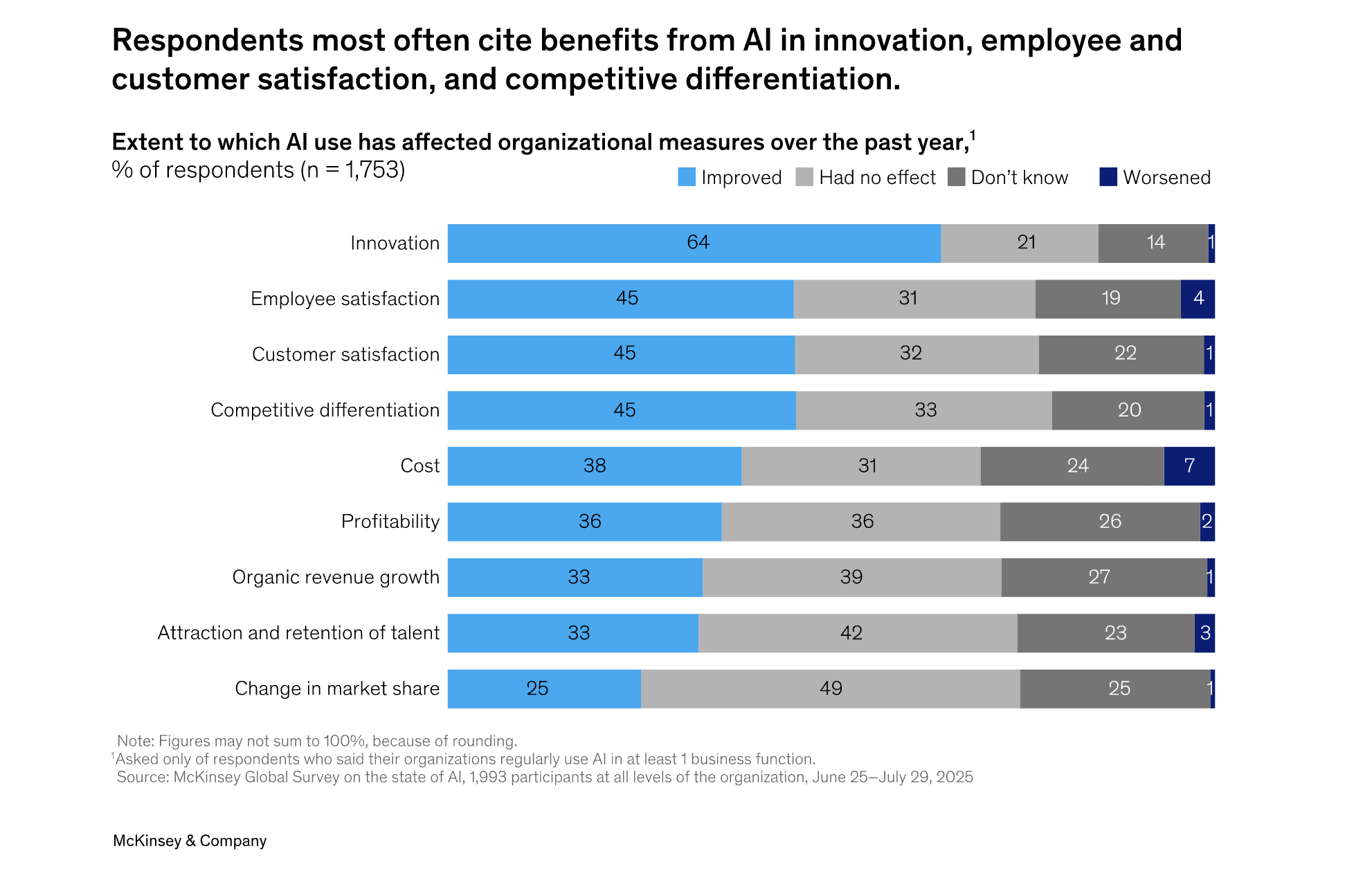

The wide disparity in ROI claims and why they exist

Depending on which report one reads, AI is either delivering extraordinary economic value or failing almost entirely to meet organisational expectations. McKinsey’s State of AI research (2024–2025) shows rising adoption and increasing value creation across multiple functions. Google Cloud’s 2025 findings point to rapid payback where objectives are clear and executive sponsorship is present. Microsoft’s AI business value studies go further still, claiming $3.5 returned for every $1 invested, an astonishing ratio by any enterprise benchmark.

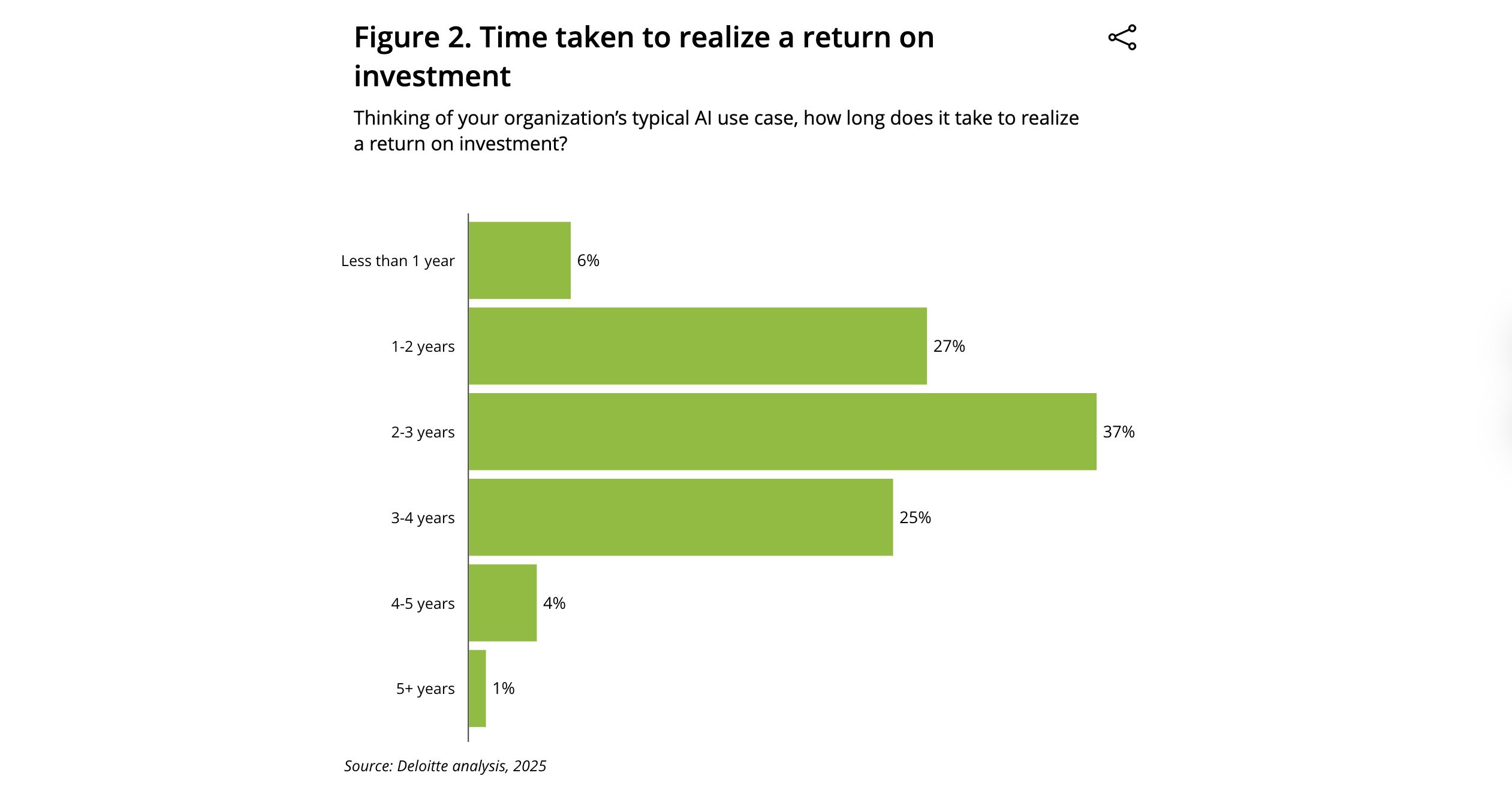

Contrast this with the other end of the spectrum. Deloitte’s AI ROI Paradox (2025) notes that only six percent of organisations achieve payback within a year, and almost all struggle to quantify benefits with any rigour. BCG’s Closing the AI Impact Gap reports that 74 percent of companies grapple to achieve or scale value despite significant AI investment. And then comes the headline-grabbing statistic from recent MIT research, cited by Fortune, that 95 percent of generative AI pilots fail to deliver ROI.**

At first glance, these findings appear irreconcilable. But when viewed together, a pattern emerges.

Both OpenAI’s usage data and Google Cloud’s ROI analysis point to a steep maturity curve. The organisations seeing consistent returns are not simply using more AI, they are using it differently. In Google Cloud’s data, enterprises that have moved into more agentic, workflow-embedded deployments are dramatically more likely to report ROI than those still confined to task-level experimentation. These early adopters deploy AI at scale, integrate it into core processes, and allocate a material share of their future AI budgets accordingly.

OpenAI’s enterprise benchmarks tell the same story from a different angle. Frontier workers engage more frequently, perform exponentially more analytical and coding tasks, and generate far higher volumes of output than median users. Leading firms send seven times more messages to GPTs than their peers, signalling a widening gap in how deeply AI is embedded into day-to-day work.

In other words, the ROI is real, but it is highly conditional. Value accrues disproportionately to those organisations that have built the structural, cultural, and operational conditions required to capture it.

What the data actually shows about AI’s economic impact

Beyond the conflicting headlines, several core truths emerge across the research landscape.

First, productivity gains are undeniable. They appear consistently across OpenAI, McKinsey, IBM, and Google Cloud. Workers are moving faster, producing higher-quality output, and completing tasks previously outside their skill set, including coding, analysis, troubleshooting, and automation. Productivity remains the most widespread and reliable category of AI value.

But productivity alone is not enough. As CFOs are quick to point out, time saved only becomes ROI when it is converted into cost transformation, throughput gains, cycle-time compression, or revenue uplift.

Second, revenue-linked ROI is emerging more clearly than in previous years. Customer-facing environments show particularly strong results. Lowe’s reports conversion rates more than doubling when customers engage with its generative AI assistant (Lowe’s x OpenAI). Intercom’s Fin Voice resolves more than half of inbound support calls, reducing operating costs and accelerating resolution. Indeed’s AI-powered matching tools improve hire quality and increase successful placements.

Google Cloud’s 2025 data complements these case studies, showing that more than half of executives reporting revenue growth attribute increases of 6–10 percent in annual revenue directly to generative AI initiatives.

Third, broader business performance indicators are beginning to shift. BCG’s analysis shows AI leaders outperforming peers across revenue growth, EBIT margin, shareholder returns, and intellectual property creation. While attribution remains imperfect, the correlation is strengthening.

Fourth, AI is changing who performs technical work. OpenAI’s surveys show that 75 percent of workers report being able to complete tasks they previously could not, including coding and data analysis. Google Cloud’s findings echo this, highlighting the redistribution of capability across functions as AI agents take on more complex workflows. This form of organisational upskilling-on-demand remains one of the least measured, yet potentially most consequential, drivers of long-term ROI.

Taken together, the evidence suggests that AI is creating value across multiple dimensions. What is missing is not impact, but the mechanisms to convert that impact into durable financial returns.

The common failure: ROI measurement has not kept pace with adoption

This brings us to the heart of the problem. The issue is not that AI lacks impact. It is that impact is rarely measured in a way that aligns with enterprise value creation.

Across the sources reviewed, five systemic gaps recur.

First, there is no standardised definition of AI ROI. Organisations track time saved, cost avoided, revenue gained, throughput increased, and employee satisfaction improved, but almost never in a comparable or finance-aligned way.

Second, productivity gains frequently fail to translate into financial outcomes because organisations do not redesign workflows, roles, or decision rights around AI-generated capacity. Tasks are automated, but operating models remain unchanged.

Third, the credibility gap between data and finance persists. CFOs are increasingly sceptical of soft metrics and anecdotal wins. They want attribution, traceability, and P&L impact, and most AI programmes still struggle to provide it.

Fourth, value is heavily skewed toward a small subset of enterprises. Statistical averages obscure the reality that perhaps 5–10 percent of organisations capture the majority of returns. These outperformers share common traits: deeper workflow integration, stronger governance, higher literacy, and visible executive sponsorship. Google Cloud’s research shows that C-suite alignment is one of the strongest predictors of reported ROI.

Finally, the people and organisational side of AI remains under-measured. The patterns associated with high ROI (integration depth, workflow standardisation, leadership commitment, data readiness, continuous evaluation, and deliberate change management) are consistently identified across reports, yet rarely appear in formal ROI frameworks.

If AI ROI feels elusive, it is because most organisations are still measuring the wrong things.

What Chief Data & AI Officers must do differently to get value

The path forward requires a shift from AI adoption to AI accountability, from counting use cases to measuring value. Senior data leaders increasingly need frameworks that distinguish between productivity, workflow impact, business outcomes, and capability building, because these domains interact and compound differently.

AI ROI cannot be reduced to a single percentage any more than enterprise transformation can be reduced to a single KPI. It must be assessed as a portfolio of interlinked value streams, each tied explicitly to strategic objectives.

This means quantifying cycle-time reduction in underwriting, not simply stating that “AI speeds up analysis.” It means tracking cost-to-serve compression in contact centres, not just reporting improved call resolution. It means measuring uplift in customer lifetime value from AI-driven personalisation, rather than relying on anecdotal engagement metrics. And critically, it means assessing the maturity of organisational capabilities, from literacy, integration depth, governance to evaluation discipline, that determine whether AI investments will continue to compound.

The frontier firms identified across OpenAI, Google Cloud, and BCG are not simply using AI more. They are using it differently. Their operating models assume intelligence embedded across workflows, not appended to them. They invest in the connective tissue: data pipelines, tool integration, governance, and measurement. They build literacy at scale. They redesign processes rather than layering AI onto legacy ones. And they understand that the return on AI is not a byproduct of technology, but of organisational readiness.

A turning point for enterprise AI

The coming year will be decisive. Enterprises have invested heavily, regulators are paying closer attention, and boards are sharpening their expectations. The promise of AI is no longer enough, performance must now be proven.

Yet one conclusion emerges consistently across the evidence: AI ROI is real. It exists in productivity, customer experience, operational economics, revenue uplift, and increasingly in structural business performance. What is missing is not impact, but the systematic capture, measurement, and conversion of that impact into enterprise value.

In that gap lies both the mandate and the opportunity for the modern CDAO. AI will not deliver ROI on its own. But with the right operating models, measurement frameworks, literacy initiatives, and workflow redesign, it can become one of the most powerful drivers of value creation the enterprise has ever seen.

And the leaders who make that shift now will define the competitive frontier for the next decade.

Related blog posts

.png)

.png)

.png)

.png)

.png)

.png)

.png)

Unlock the power of your data & AI

Speak with us to learn how you can embed org-wide data & AI fluency today.